CFA财务报表分析练习题"Financial Report":Rev-aluation model

财务报告与分析中章节的设置是循序渐进、逐层深入的,前面介绍的术语在后面还会有详细的解释与探讨。

由于财务报告与分析本身自立体系,它是上市公司和报表使用人之间沟通交流的语言,所以学起来与外语学习有几分相似。

财务报告与分析一共分为四大部分:

第一部分是扫盲阶段,主要介绍财务术语、体系等基本知识。

在此基础上,第二部分更深入地讲解财务报表编制以及财务报表分析的方法。

进一步地,第三部分针对存在利润操纵空间的重点科目做详细、深入的讨论。

最后,第四部分是前面三部分内容的综合应用。

四大部分在考试中占比最大的是第二部分和第三部分,大概占财报分析所有题目的80%以上。其次是第一部分,占比10%左右。

由于第四部分是财务分析的综合应用,不太适合一级的出题形式,所以

出题比例相对比较少,大概占5%左右。

Questions 1:

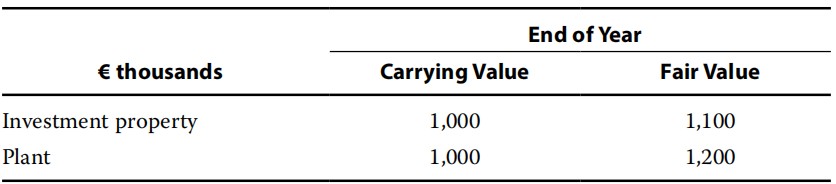

A company that reports in accordance with IFRS does not use the cost model to value its investment properties and property,plant,and equipment.Information related to an investment property and a plant is as follows:

The impact on its net income for the year will most likely be a gain(in thousands)of:

A、€100.

B、€300.

C、€200.

【Answer to question 1】A

【analysis】

A is correct.The fair value model would be used for the investment property,and the€100 thousand gain should be recognized on the company’s income statement.The r*uation model would be used for the plant,and the€200 thousand gain should be recognized in the r*uation surplus account on the balance sheet with no impact on net income.Therefore,only the€100 thousand will affect net income.

B is incorrect.The r*uation model would be used for the plant,and the gain should be recognized in the r*uation surplus account on the balance sheet.This is a new purchase and therefore no gains need to be recognized on the income statement to reverse previously recognized losses.Therefore,a maximum of$100,000 would be recognized on the income statement.

C is incorrect.The r*uation model would be used for the plant,and the gain should be recognized in the r*uation surplus account on the balance sheet.This is a new purchase and therefore no gains need to be recognized on the income statement to reverse previously recognized losses.

Questions 2:

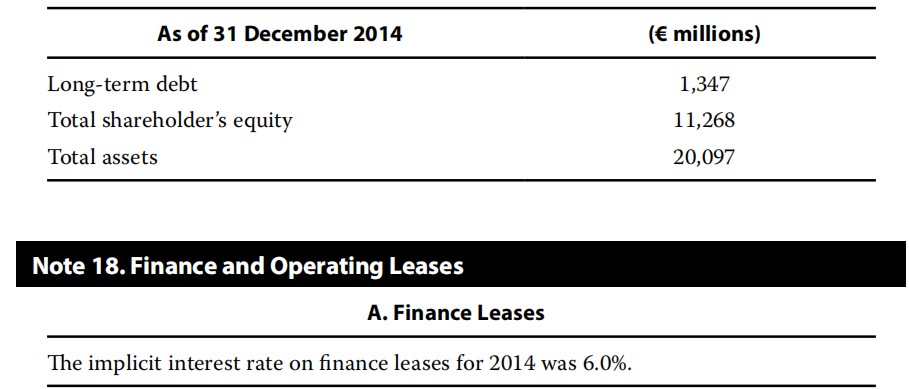

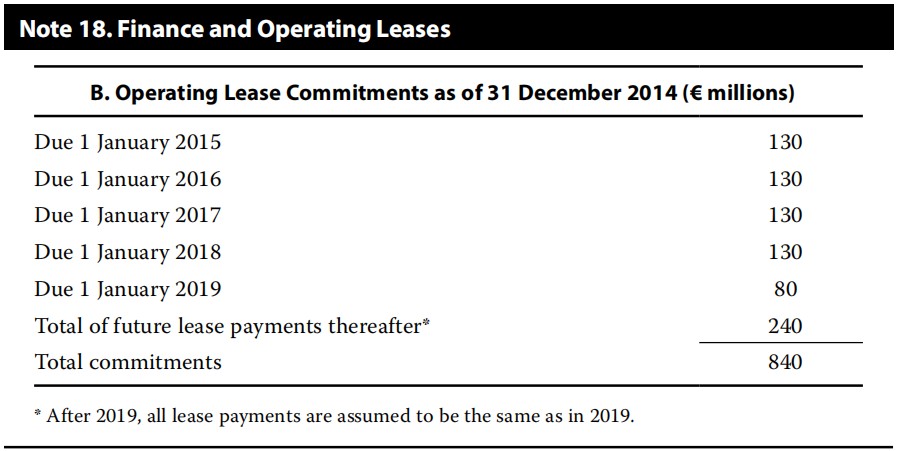

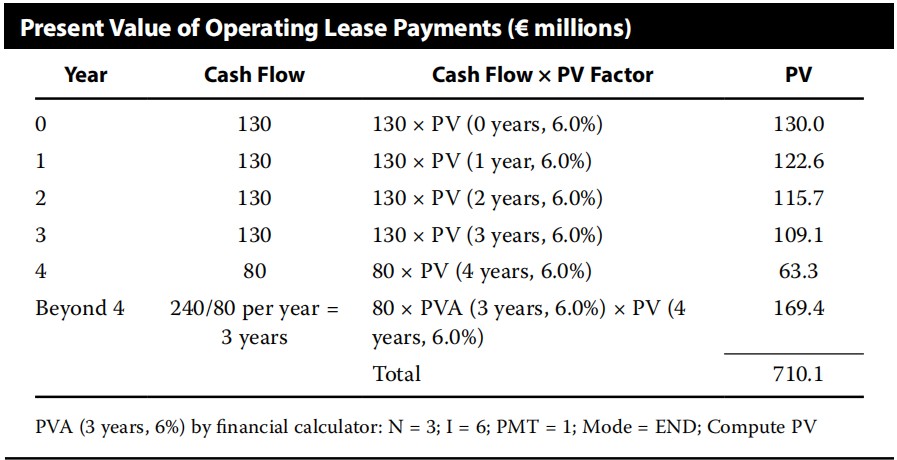

The following is selected balance sheet data for a company along with information about its financial and operating lease obligations.

If the company were to capitalize its long-term leases,its adjusted long-term debt-to-assets ratio as of the end of December 2014 would be closest to:

A、9.9%.

B、10.2%.

C、10.4%.

【Answer to question 2】A

【analysis】

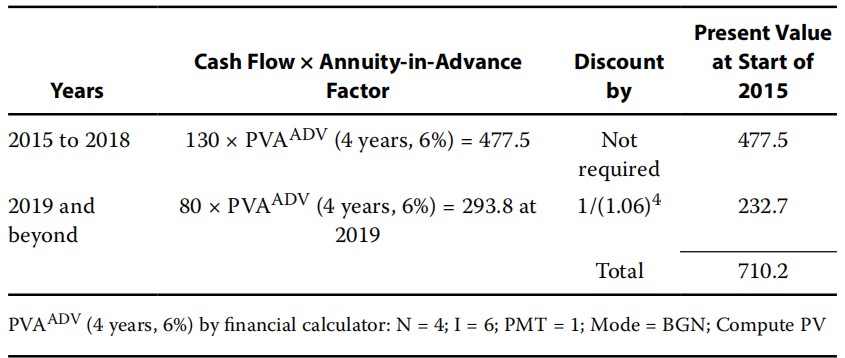

A is correct.If the leases were capitalized,both total assets and liabilities would increase by the present value of the lease payments.The lease commitments after 2019 are assumed to be the same as in 2019,so there are estimated to be 240/80=3 additional payments.The present value of the operating lease payments can be calculated as the sum of the present values of two annuities-in-advance(PVAADV):a four-year annuity starting immediately(beginning of 2015)and another four-year annuity starting in four years(2019)

Adjusted long-term debt/asset ratio calculation:

Adjusted long-term debt:1,347+710=2,057

Adjusted total assets:20,097+710=20,807

Adjusted long-term debt/asset ratio:2,057/20,807=9.9%

Alternatively,the individual cash flows can be separately discounted.

B is incorrect.Adding PV(Operating lease)only to debt:2,057/20,097=10.2%.

C is incorrect.The undiscounted total commitments are added to both assets and long-term debt:Adjusted debt ratio=(1,347+840)/(20,097+840)=10.4%

版权声明:本条内容自发布之日起,有效期为一个月。凡本网站注明“来源高顿教育”或“来源高顿网校”或“来源高顿”的所有作品,均为本网站合法拥有版权的作品,未经本网站授权,任何媒体、网站、个人不得转载、链接、转帖或以其他方式使用。

经本网站合法授权的,应在授权范围内使用,且使用时必须注明“来源高顿教育”或“来源高顿网校”或“来源高顿”,并不得对作品中出现的“高顿”字样进行删减、替换等。违反上述声明者,本网站将依法追究其法律责任。

本网站的部分资料转载自互联网,均尽力标明作者和出处。本网站转载的目的在于传递更多信息,并不意味着赞同其观点或证实其描述,本网站不对其真实性负责。

如您认为本网站刊载作品涉及版权等问题,请与本网站联系(邮箱fawu@gaodun.com,电话:021-31587497),本网站核实确认后会尽快予以处理。

更多服务

更多服务